Retirement can be the most rewarding chapter of your life — but it can also be the most financially vulnerable. Without a steady paycheck, market downturns and inflation can feel far more threatening. Many retirees focus solely on protecting against stock market losses, but an equally dangerous long-term threat is the quiet erosion of your purchasing power — also known as currency debasement.

In Boston and across New England, where the cost of living is already high and property taxes can be significant, retirees must be intentional about protecting their savings from both types of risk.

1. Understanding Market Volatility in Retirement

The concept: Market volatility refers to the swings in value of your investments. A 20% market drop might not rattle a 35-year-old investor with decades to recover, but it can be much harder to weather in retirement — especially if you’re regularly withdrawing funds to cover living expenses.

Example: Susan, a retired teacher living in Wakefield, Massachusetts withdrew $60,000 per year from her portfolio. In her second year of retirement, the market dropped 25%. Because she still needed the $60,000 for living expenses, she had to sell more shares at lower prices — permanently locking in the losses. Without a buffer, her portfolio recovery lagged for years.

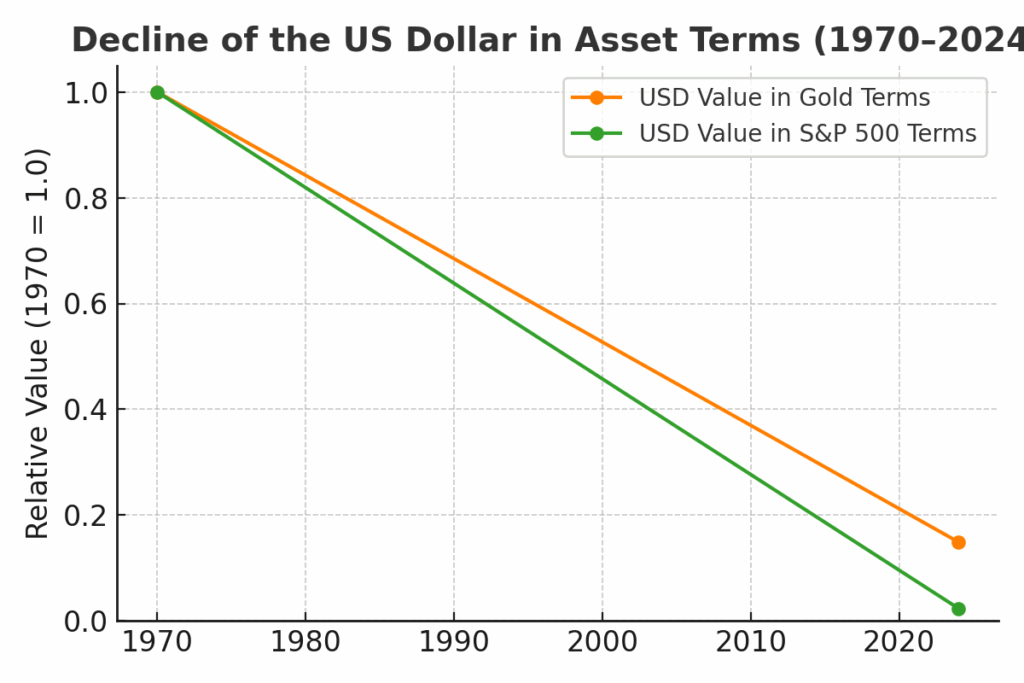

2. The Other Risk: Currency Debasement

The concept: Most people think of inflation as the rising price of goods. Currency debasement is the flip side — the declining value of the dollars you hold, especially when measured against other assets you could own instead.

Example: Jim and Linda, from Swampscott, kept $500,000 in cash after selling a business. They felt secure avoiding the stock market’s ups and downs. But over the next decade, even at moderate inflation, the purchasing power of that $500,000 fell by nearly 25%. When measured in gold and the S&P 500, the “value” of their cash dropped over 50%, meaning they could have bought far fewer shares or ounces than before.

Over the last 50 years, the U.S. dollar has lost more than 80% of its value compared to gold and the S&P 500. Even without a crash, sitting on too much cash for 7–10+ years can quietly erode wealth.

3. Striking the Right Balance Between Safety and Growth

The concept: To protect against market losses, many retirees keep a portion of their portfolio in “safe” assets like cash, CDs, and short-term bonds. This makes sense — you need accessible funds for near-term spending. But to protect against currency debasement, you also need growth-oriented assets that outpace inflation.

Growth assets can include:

- Stocks (U.S. and international)

- Real assets like real estate or commodities

- Inflation-protected securities like TIPS

Example: Paul, living in a coastal New England town, kept two years of living expenses in cash, invested 40% in bonds, and 40% in stocks. This mix allowed him to cover short-term needs without panic-selling in downturns, while his growth assets helped his portfolio keep pace with rising living costs in his area.

4. The “Cash Bucket” Strategy

The concept: A “bucket” strategy helps balance safety and growth:

- Bucket 1: Cash & short-term bonds for 1–3 years of expenses.

- Bucket 2: Moderate-risk investments for years 3–7.

- Bucket 3: Long-term growth investments for needs 7+ years out.

Example: Mary and Alan, retirees in Boston’s South End, used a bucket strategy during the 2020 downturn. They lived off Bucket 1 (cash and CDs) for two years without selling stocks at depressed prices. By the time they replenished Bucket 1, the market had recovered, preserving their long-term wealth.

5. Making Adjustments Over Time

The concept: Your ideal safety-growth balance changes over time. Early retirees may afford to take more growth risk. Later in retirement, it often makes sense to reduce volatility and rely more on predictable income streams.

Example: George, a retired engineer from Cambridge, started retirement at 62 with 65% in stocks. As he approached 75, he shifted to 45% stocks, 40% bonds, and 15% cash. This let him keep some growth potential while making his income stream more predictable — especially important as health costs rose.

6. The Bottom Line

Managing volatility in retirement isn’t just about avoiding the next market crash — it’s about preserving your ability to live well for decades, even as the value of the dollar declines. A thoughtful plan should:

- Provide enough short-term safety to weather downturns.

- Maintain long-term growth to fight inflation and debasement.

- Adjust over time as your needs and the markets change.

Example: In a Boston suburb like Wellesley or Concord, where property taxes and living costs are high, having a portfolio that’s only “safe” could be as risky as one that’s too aggressive. The key is balance — protecting today while preparing for tomorrow.