Appointment Confirmed!

Next steps, quick facts, and a few ways to prepare so our meeting is as valuable as possible

What to Expect in our Meeting

Whether you come with detailed numbers or just a few big questions, you’ll walk away with clarity

Whether you arrive with detailed numbers or just a few big questions, you’ll leave with more clarity and direction.

This first meeting is completely no-cost and no-obligation. We can dive deep into your financial picture or simply explore the areas you’re most curious about — whatever feels right for you. Some people bring full account details and goals, while others prefer to keep the discussion high-level. Both approaches are perfectly welcome.

If you’d like to share some personal financial information in advance, feel free to complete the Evergreen Financial Profile Form below.

Evergreen Financial Profile Form

You can take our time together in whichever direction works best for you:

- Detailed & Specific: Share your financial picture (accounts, balances, goals) and we can explore whether Evergreen is the right fit for you.

- High-Level & Exploratory: Keep it broad, ask questions, and get a feel for how I approach retirement planning, investments, and taxes.

- Combination: Start with a few key questions and decide how much detail you’d like to share as the conversation unfolds.

- Your Zoom link or location details will be sent directly to your email provided

Quick Facts About Evergreen

Here’s what makes us different (and what we don’t do):

- One Flat Monthly Fee — All-Inclusive

Investment management (for any accounts you have us manage) and comprehensive financial planning are both included. No extra charges, no commissions, no hidden costs. - Not Hourly or Project-Based

While there’s no long-term contract, our goal is to be your ongoing advisor — not just a one-time or short-term fix. - Built for Long-Term Partnerships We work best with clients who want a dedicated advisor to guide them through retirement and beyond.

- Clear Relationship Requirements

We manage client accounts directly at Charles Schwab, and ask that at least $500k be managed with us. Beyond that, you’re welcome to keep other accounts elsewhere if that makes sense for you. - Simple, Convenient Billing Your flat fee is billed directly from your Charles Schwab account each month. We don’t accept checks or credit cards — this way everything is streamlined, secure, and accounts are billed in a transparent way based on our contract.

How often can we meet?

We can meet as often as needed, especially early on while transferring accounts, placing trades, and modeling retirement scenarios. That phase typically includes more frequent check-ins to keep things on track.

We prefer in-person meetings to build a strong relationship, but we’re happy to hop on a Zoom or quick call when something urgent comes up. After onboarding, we’ll set a communication plan that fits your preferences.

How are fees charged?

Once your accounts are set up at Charles Schwab, we’ll work with you to decide which account(s) you’d like us to bill. Fees are automatically deducted from your managed Schwab brokerage accounts at the beginning of the month, charged in advance. Spouses can choose to split fees between accounts if preferred.

We do not accept payment by credit card or check.

Do you charge a separate fee to manage my investments?

No! Our flat fee includes investment management of any accounts you want to offload to us as well as all financial planning and consultations.

What is the difference between fee-only and a flat fee?

Fee-only can mean different things, from project-based financial planning with upfront costs, to percentage-based models, per-plan fees, and hourly rates. We take pride in our straightforward approach, focusing on simplicity and common sense approach.

Do you work by the hour or on a project base?

No. Our philosophy is based on building long-term relationships for individuals and families that would like help throughout many phases of life, and we don’t believe the hourly model fits that philosophy.

Are you a fiduciary?

Yes! We take the fiduciary model one step further. Being a fiduciary means advice should not result in more compensation to the advisor. While this is can be true of advisors charging a percentage of assets, the nature of the calculation can lead to a conflict of interest.

Are you a Certified Financial Planner, CFP®?

Yes! The CERTIFIED FINANCIAL PLANNER (CFP) designation serves as an official acknowledgement of expertise in crucial areas such as financial planning, taxes, insurance, estate planning, and retirement. This recognition is owned and conferred by the Certified Financial Planner Board of Standards, Inc. Individuals who fulfill the requirements, including passing the CFP Board’s initial exams, are granted the designation and are committed to participating in continuing education programs to uphold their skills and certification.

I own individual stocks. Can I still work with you given your index fund approach?

Yes! While our core investment models are built around index funds, we understand that some clients prefer to maintain a portfolio of individual stocks. If you’d like to keep your stock portfolio intact while receiving our guidance and making adjustments over time, we’re happy to work with you.

What makes you different from other advisors?

Evergreen offers the best of both worlds—personalized service with big-firm resources. You’ll work directly with a seasoned investment advisor with 18 years of experience, backed by cutting-edge technology that provides the same tools and security as major firms. As a boutique, growing firm, we prioritize personal relationships and tailored guidance. Best of all, we provide comprehensive investment management and advice for one transparent, flat fee.

Who is Evergreen NOT a great fit for?”

- Market Beating Seekers – Evergreen’s investment approach is rooted in index-based strategies, built on the belief that markets deliver strong returns over the long run. If you’re seeking consistent outperformance every year, regardless of market conditions, we may not be the right fit.

- New Investors – Evergreen is focused on helping individuals within 10 years of retirement. Given the nature of our flat-fee model, new investors with little savings would pay too much for it to make sense. We encourage younger investors to keep their costs as low as possible as they build assets. With that said, if you are a young investor with questions on starting out and need some help, send us an email and we’ll schedule a one-time call free of charge to help you get launched.

- Ultra-high net worth clients – Clients and families with ultra-high net worth that are used to paying an advisor to be the advisors top priority each week. With respect to our other clients, we aren’t able to monopolize the majority of our time to one family. We also do not offer private equity, venture capital, or other alternative investments.

Can you advise me on my workplace 401(k) account?

Yes! While you typically can’t roll over your workplace 401(k) to an IRA while still employed, we can help you navigate your plan’s fund options and identify the low-cost choices available. Every 401(k) plan has unique rules and investment selections, so we’ll work with you—whether by reviewing your online portal or calling the provider directly—to gather the necessary details and provide tailored advice.

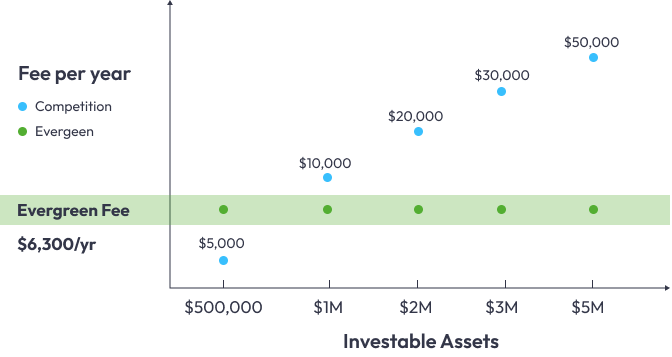

The Evergreen Fee Model Compared to the AUM 1% Advisors